Does your income protection insurance cover you for loss of job?

The recent emphasis on job insecurity may have prompted some to rush out and purchase income protection cover (disability income protection insurance). Many may have mistakenly assumed they were protecting themselves from the risk of future unemployment.

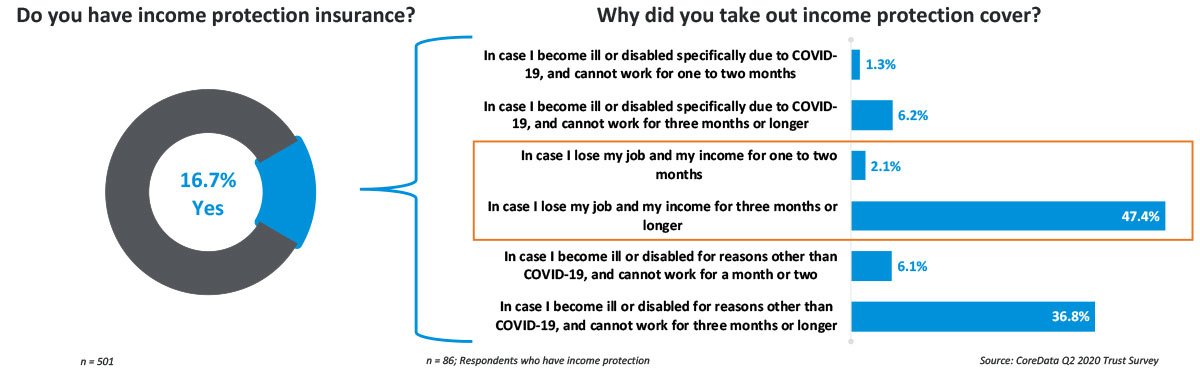

Research in April 2020 found that nearly half (49.5%) of Australians surveyed who had income protection insurance mistakenly believed they would be covered in the event of job loss[i]. It revealed that of the 16.7% of respondents who had income protection insurance, nearly half took out this insurance in case they lost their job and income.

What does income protection insurance cover?

DII, (also known as income protection insurance) is designed to pay up to 85% of your pre-tax income for a specified period of time is you’re unable to work due to partial or total disability.

Income protection insurance does not cover you for lost income because you are stood down or become unemployed.

This highlights the importance of understanding exactly what it is you are purchasing, before you buy insurance.

Understand what you are buying

It is critical you are not buying an insurance policy you wouldn’t have taken out if you’d understood what it covered.

Unlike policies in the United States and United Kingdom, income protection in Australia from life insurance companies will not provide a benefit payment if the policyholder is involuntarily unemployed or made redundant[ii]. In fact, it is actually illegal for life insurance providers to pay out in these circumstances[iii].

There are insurances that pay out if you lose your job

But disability income insurance (DII) isn’t one of them.

For example, unemployment cover benefits are often bundled up as part of a loan protection plan and intended to pay out, after a designated wait period, if you become ‘involuntarily unemployed’, due to redundancy or retrenchment, from full time-time employment. Some insurers offer redundancy insurance as an add-on with their income protection policies.

Numerous benefits and exclusions may apply to each different type of insurance policy. Different policies have different monthly benefits and benefit periods. They may also have no claim periods (e.g., you must have held the policy for 6 months) and waiting periods before you can claim. It’s important to understand these as different policies and options will be suitable for different situations.

Financial planners can assist you by providing expert advice to compare the range of policies on offer and find the most suitable policy to suit your circumstances.

Want to know more?

1) You can click here to book a free 15-minute free clarity call with Sam Woodhouse to discuss how this may relate to you.

2) Join our Your Money Simplified email list to start taking control of your money today. And when you subscribe, I'll give you a PDF called My 3-Step Process for Building Your Road Map to Financial Freedom.

The information contained in this article is general information only. It is not intended to be a recommendation, offer, advice or invitation to purchase, sell or otherwise deal in securities or other investments. Before making any decision in respect to a financial product, you should seek advice from an appropriately qualified professional. We believe that the information contained in this document is accurate. However, we are not specifically licensed to provide tax or legal advice and any information that may relate to you should be confirmed with your tax or legal adviser. [i] https://www.coredata.com.au/blog/misperceptions-about-ip-cover-a-red-flag-for-life-industry/ [ii] https://www.finder.com.au/income-protection/redundancy[iii] https://www.finder.com.au/loss-of-job-insurance