5 ways to save for your children’s education

A key financial priority for many of us is supporting the education of our children.

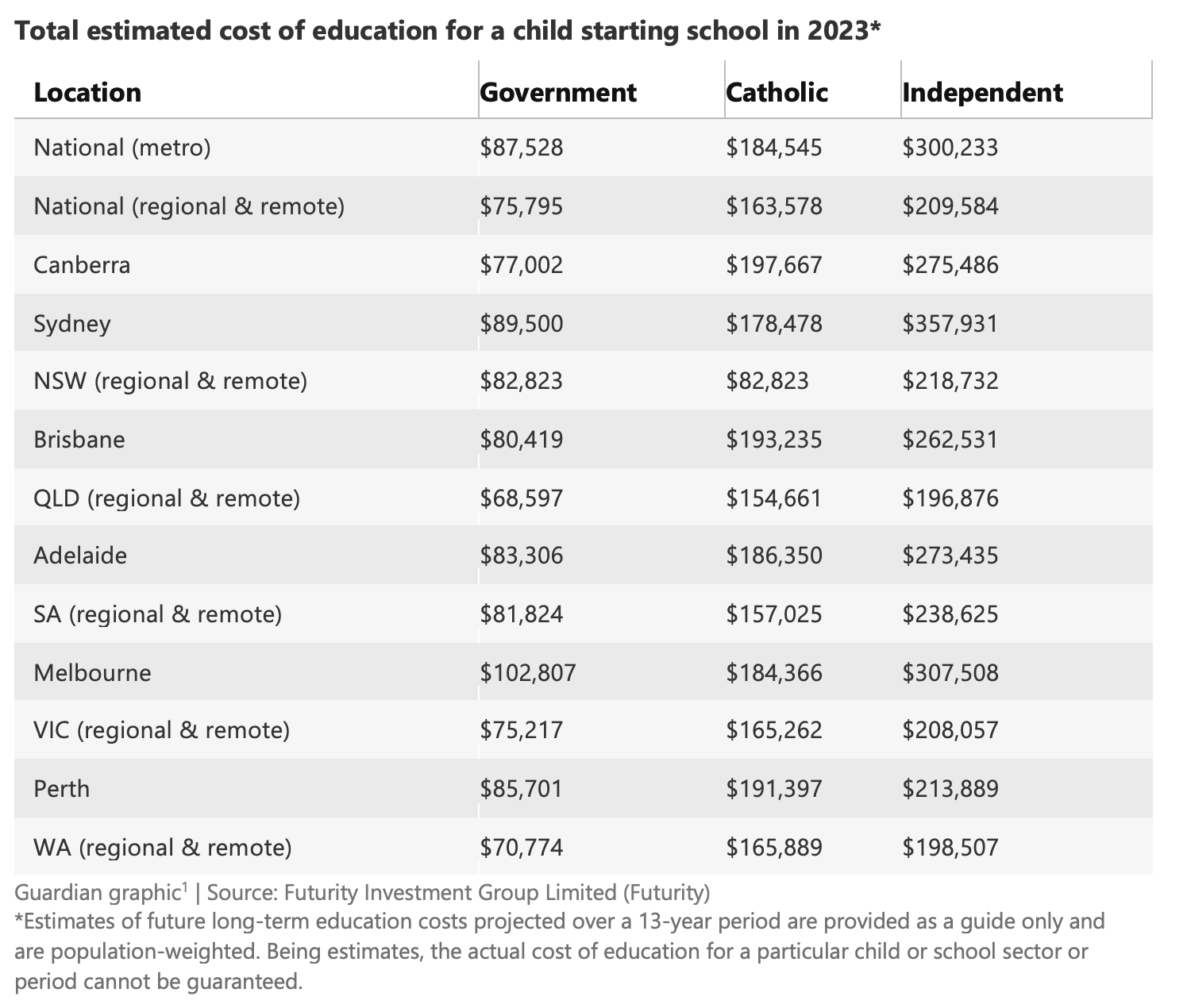

We are lucky in Australia to have a strong education system, and whether you choose public, private or independent schooling or are looking at supporting their tertiary education, the goal is the same: to set your children on the path to a bright and rewarding future.

Education costs are broader than school fees alone, with outside tuition, school camps, transport, uniforms, electronic devices, and sports equipment all adding up.

Each choice involves a much different financial investment. What you choose will come down to your own view of what is best for your children. Regardless of your choice, a range of financial options and savings are available to support your children’s education needs.

Weighing up your options

The golden rule for most financial plans is to establish and implement your plan as soon as possible. More time will help you maximise your returns and boost your savings. With that in mind, here are five options you might consider:

1. Take advantage of a home loan offset account

An offset account is a bank account linked to your home loan. Using it to save for your children’s education can be tax-effective and reduce the interest paid over the term of your loan.

Effectively, any money saved in the account earns an after-tax interest rate equal to the home loan rate, which is usually substantially higher than interest received taxed at your marginal income tax rate, as offered on term deposits or similar.

Self-discipline is the big challenge in using an offset account.

2. Investment or education bonds

Investment bonds are investments through which you lend money to a government or company for potential capital growth and tax benefits . There is usually a minimum amount you must invest. The tax rate on investment bond earnings is up to 30%, which is advantageous for higher-income earners. Usually, subject to certain rules, if you hold investment bonds for at least 10 years, your entire investment earnings will be ‘tax-paid’, and withdrawals after this date will be free of personal tax.

Education bonds are a special type of investment bond that must be intended for the purpose of saving for education. Education bonds include the features and tax advantages of conventional investment bonds plus additional educational tax advantages, estate planning features, and the freedom to designate numerous beneficiaries.

3. Term deposits

Term deposits are one of the most well-understood and simplest ways of earning interest on savings. They offer a fixed interest rate over a specified period, typically for one or two years. On termination, you can choose to roll them over into a new term deposit, understanding that a new interest rate will apply, which may be lower.

4. Managed or Exchange Traded Funds (ETFs)

Investing in a managed fund could be a reasonable option if you want to invest over a reasonable term, say three to ten years.

You could invest in a managed fund with exposure to the share market, property or fixed-income assets, or a diversified asset allocation. They generally require you to have a minimum amount of money already available to invest, and you may incur an establishment fee. There are also ongoing investment management fees.

Some managed funds are listed on the Australian Stock Exchange (ASX) and are known as Exchange Traded Funds (ETFs). They can be bought and sold like other ASX shares, meaning you can easily increase your holding as you can afford it, or sell if needed.

Capital Gains Tax (CGT) is usually applicable when you sell.

You should read and understand the risks and returns expected from these investments over the timeframe you’re planning to invest.

5. Invest tax-effectively

If you’re investing with a partner, it might be worth considering in whose name you should invest your funds. It can be more effective to invest in the name of the person paying the lowest rate of income tax. You should note to monitor and review this should a job change or promotion alter your relative tax situations or if your relationship changes.

Setting up for success

If you’re starting early, saving for education will be a medium to long-term effort, so some of the investment options listed above may experience periods of negative returns. This possibility suggests that reducing risk while optimising your savings over a five to 10-year timeframe might call for some diversification of your investment portfolio – allocating your savings across several types of investment.

Want to know more?

1) You can click here to book a free 15-minute free clarity call with Sam Woodhouse to discuss how this may relate to you.

2) Join our Your Money Simplified email list to start taking control of your money today. And when you subscribe, I'll give you a PDF called My 3-Step Process for Building Your Road Map to Financial Freedom.

The information contained in this article is general information only. It is not intended to be a recommendation, offer, advice or invitation to purchase, sell or otherwise deal in securities or other investments. Before making any decision in respect to a financial product, you should seek advice from an appropriately qualified professional. We believe that the information contained in this document is accurate. However, we are not specifically licensed to provide tax or legal advice and any information that may relate to you should be confirmed with your tax or legal adviser.[1] https://www.theguardian.com/australia-news/2023/jan/25/free-public-education-costs-as-much-as-100000-in-parts-of-australia-report-finds